Such investor behaviour is indicative of a climate ripe for class actions by concerned shareholders to ensure the companies they are invested in produce and stick to appropriate climate policies and targets; and pay the price if they do not. There is already a significant uptick in such claims and associated types of action with similar aims.

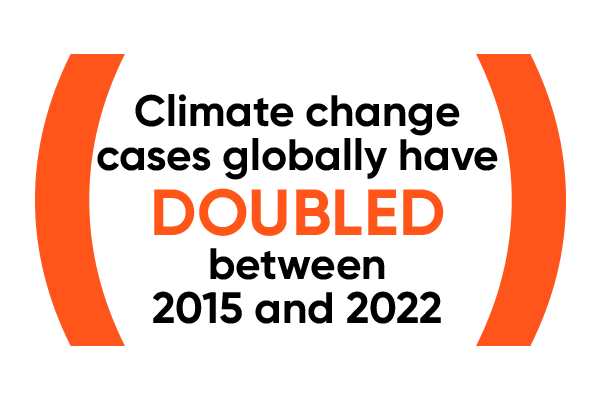

Analysis by the London School of Economics (LSE) of the Grantham Research Institute’s Climate Change Laws of the World database showed the number of climate change cases globally had doubled between 2015 and 2022, and a quarter of the more than 2,000 claims in that period were filed between 2020 and 2022.

While the majority of cases are brought against governments, the database lists 135 claims against companies to date. Albeit that these corporate claims are currently still mostly in the US, the UK is fast catching up. Australia and the UK are the biggest fora for climate change litigation outside the US, with 124 and 83 cases filed respectively to date, according to the LSE.

Derivative actions

It is easy to see how, if the climate change resolution tabled is not passed, or if the company continues to employ a climate strategy that the activist investor disagrees with, the issue might be escalated to the courts through an individual claim, or increasingly by way of class action.

In February 2023 ClientEarth, an organisation that uses legal claims to fight climate change, and which is a shareholder in Shell plc, issued a derivative action on behalf of the company against Shell’s 11 directors, alleging they were in breach of their duties as directors under the Companies Act by failing to adopt and implement an energy strategy that aligns with the Paris Agreement.

Derivative claims require permission from the court to proceed and on 12 May 2023 the English High Court rejected ClientEarth’s application for permission, deciding on the basis of the written submissions that it had received that there was no prima facie case to give permission. The court found the majority of Shell’s shareholders were supportive of the directors’ strategic approach to climate change risk, and those expressing support of ClientEarth’s case were a “very small proportion of the total shareholder constituency”. ClientEarth sought and obtained permission for their application to be heard before the court, enabling them to make oral submissions. This hearing took place on 12 July 2023, and on 24 July 2023 the court handed down a judgment maintaining its decision to dismiss the claim. ClientEarth has indicated that it intends to appeal this decision.

A year earlier, two academics with some crowd funding support attempted to bring a derivative action against the corporate trustee of their pension fund, alleging that the directors had breached their duty by failing to create a credible plan for disinvestment from fossil fuel investments and therefore prejudicing the success of the company.

The court refused to grant the claimants permission to continue the claim, in part because the claimants had not specified what the impact of disinvesting from fossil fuel would have been, and therefore were not able to demonstrate that a loss had been suffered by the company. In July 2023, the Court of Appeal upheld this decision and refused to grant the claimants permission to continue the claim.

These cases may have set a precedent for future derivative actions, forcing activist shareholders to consider their cases more carefully. However, their failure is unlikely to stop other activist groups from pursuing similar claims, not least given that their reasoning and strategy does not reflect that of your everyday litigant.

Public companies are clearly at increasing risk of their energy strategies being scrutinised and challenged in the same way. Directors of public companies may be feeling particularly vulnerable to being singled out as defendants often for strategic reasons.

It may be tempting for potential defendants to be comforted by the fact that claimants need to overcome the hurdle of the permission stage in derivative claims, but it would be foolhardy to assume that the derivative action is not going to be an effective tool in the arsenal of the class action environmental claimant going forward.

Even unsuccessful applications for permission can adversely affect the defendant company: the requirement for permission does not prevent the claim being issued, particularised and publicised. Such activist claimants also tend to have active and effective media machines.

The Financial Service and Markets Act

As well as derivative actions, activist investors also have the ability to bring claims under sections 90 and 90A of the Financial Services and Markets Act (FSMA), which stipulate that a company which has created a ‘misleading impression’ as to the market value of its shares with the result of making a gain for itself or causing a loss to others must compensate those who have suffered loss.

Section 90 covers untrue or misleading statements or omissions made in a company’s listing particulars or prospectus, while section 90A and Schedule 10A relate to misleading statements or dishonest omissions in published information such as annual reports or trading updates, or dishonest delays in publishing such information.

Although the number of section 90 and section 90A claims is so far low, we envisage activist investors increasingly bringing claims under the legislation in relation to statements made about climate change issues in public statements or publications, such as financial statements or prospectuses.

Regulator involvement

ClientEarth filed an application for judicial review in February 2023 against the Financial Conduct Authority (FCA), alleging that the FCA acted unlawfully by approving the prospectus of UK oil and gas company Ithaca Energy. ClientEarth alleges that Ithaca Energy’s disclosures in its prospectus did not adequately describe the climate-related risks faced by the company, and therefore breached statutory requirements. The court refused permission for the judicial review to proceed, but ClientEarth indicated they would be applying for the decision to be reconsidered.

While this particular claim is not brought under FSMA, and ClientEarth has been clear that it is not seeking to interfere with Ithaca’s listing, the case is an example of another tool in the armoury of the ESG climate activist.

Greenwashing Claims

Another growth area in climate litigation is claims relating to corporate ‘greenwashing’ – making misleading public statements in order to present an environmentally responsible public image. A 2023 study released by IBM found that only 20 per cent of consumers reported that they trust company statements about environmental sustainability.

Only 20 per cent of consumers reported that they trust company statements about environmental sustainability.

Among climate activists, there is a global movement to take active steps to challenge corporate greenwashing. For example, in 2019, ClientEarth submitted a complaint to the Organisation for Economic Co-operation and Development against BP’s clean energy advertising campaign. ClientEarth has also brought a claim against the airline KLM in the Netherlands in relation to its sustainable flying advertising campaigns, as part of a wider aim of achieving a ban on all fossil fuel advertising. There have also been various complaints made in the UK to the Advertising Standards Authority about FIFA’s claims that the 2022 World Cup was carbon neutral.

The growing focus on sustainability means that corporates are becoming more driven by investing in green credentials. Class action litigation is almost inevitable where green labels, descriptions and strategies turn out not to be quite so green as described or envisaged.

In this context, corporations will need to take extreme care when making public statements about environmental issues. There is potential for a wide range of claims: greenwashing relating to financial products which are marketed as green investments; pension funds or products said to be making only green investments; statements relating to a company’s general environmental credentials, strategies or policies; or, in the case of private transactions, relating to warranties and indemnities on environmental issues in an SPA.

“It’s fundamentally about checking and not saying something to the market that’s wrong,” stresses Nayer. “It’s about actually being values driven and being consistently so. If we could go further, it’s also about caring about the environments in which you work,” he adds.

Greenwashing is not just a concern for corporates. Regulators are also grappling with their role in addressing greenwashing risks. ClientEarth’s judicial review proceedings against the FCA in respect of Ithaca’s alleged failure to properly and fully describe the specific climate-related risks facing this fossil fuels company in its prospectus will likely cause the FCA to scrutinise environmental claims made by public companies in more detail. Indeed, it has recently introduced reporting requirements for listed companies.

Other regulators are stepping up their focus on ESG compliance. One said in April that it expected trustees to comply with ESG and climate reporting duties. As well as helping the world to meet climate change targets, one regulator warned that financially material ESG factors could affect a pension fund’s performance. It suggested trustees should consider developing a climate action plan clarifying the actions they have taken and plan to take to comply.

Plan Your Defence in Advance

Directors and corporations must effectively plan their response to a swiftly evolving landscape for ESG-related group actions. The risk for companies as corporate entities is well-established, but there can also be significant regulatory and reputational consequences for individuals, particularly at board-level.

Nayer emphasises the increasing pressure on corporates to demonstrate a purposeful approach to business and good stewardship through ESG measures. He highlights the challenge for companies to show they are responsible actors, with ESG serving as a measure of their commitment.

“Companies are required to be led in a more purposeful, self-aware and community-based approach. When they’re not, damage ensues,” Nayer says.

To effectively mitigate risk, companies need to anticipate potential legal challenges and devise robust strategies. This includes assessing the vulnerability of their climate change policies to challenges from activist investors.

It is essential to ensure that public statements about climate-related matters can withstand scrutiny.

Looking ahead, the ESG litigation landscape will continue to evolve, with the potential for more class actions and legal challenges. Directors and corporations must remain vigilant, adapt to emerging regulations, and proactively address ESG risks to safeguard their long-term success and reputation.