The Past

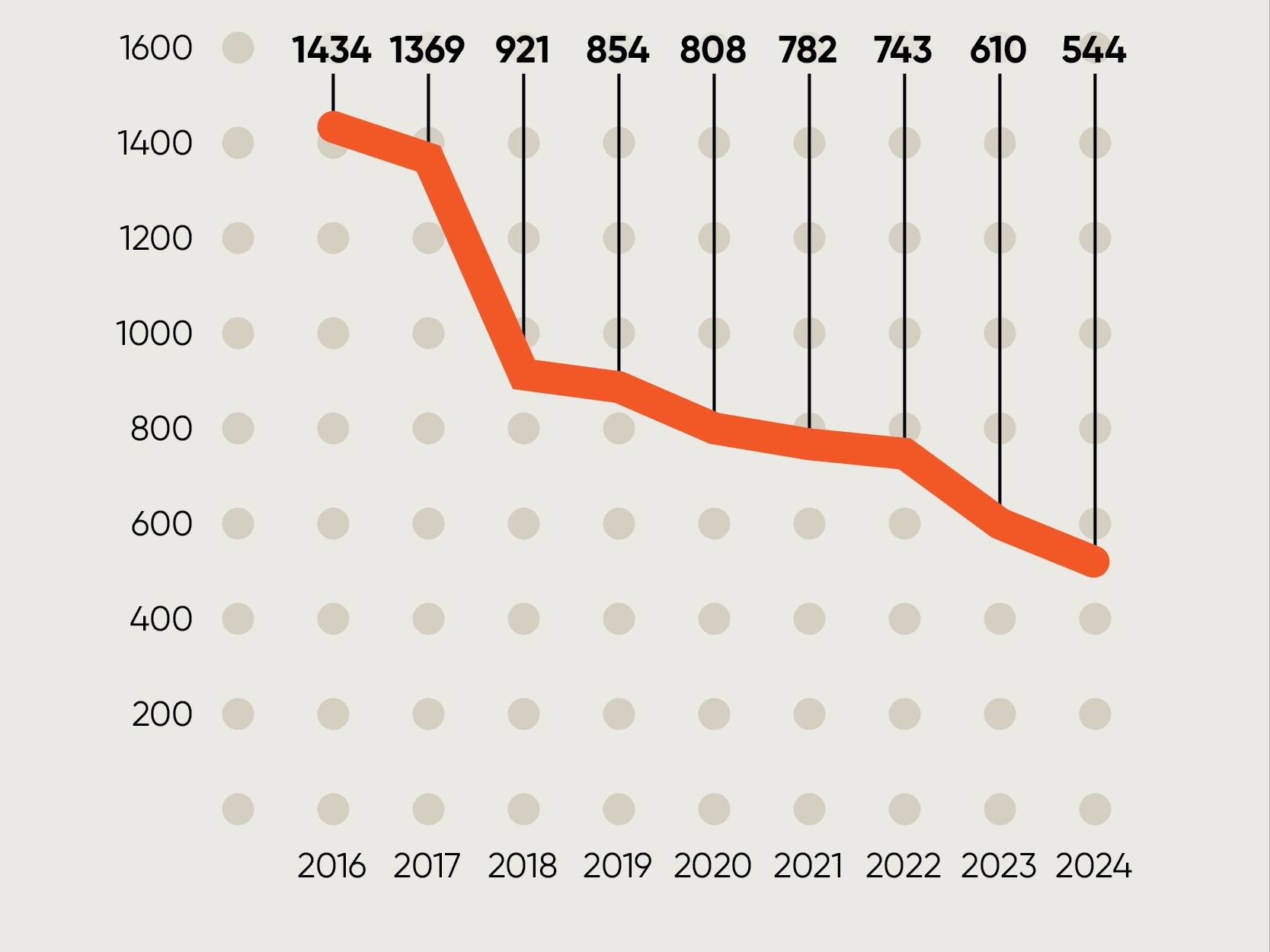

If the past is any predictor of the future, a second Trump administration is unlikely to take a hands-on approach when it comes to FINRA. The data indicates that reining in FINRA was not a priority during the first Trump administration. There was no material pullback in FINRA enforcement activity after Trump took office in 2017. The number of new disciplinary actions against firms and individuals filed in 2017 was little changed from 2016 (1,369 vs. 1,434).

While the number of actions dropped sharply to 921 in 2018, it appears that this decline was not attributable to any action taken by the Trump administration but a self-imposed pivot by FINRA. Shortly after Robert Cook became FINRA’s CEO in August 2016, he kicked off a listening tour seeking feedback from member firms and other stakeholders. The result was the launch of a self-evaluation and organizational improvement initiative in March 2017 called FINRA360. Under FINRA360, FINRA appears to have changed its approach to addressing violations by relying more on coaxing voluntary compliance through its examination function and less on formal enforcement investigations. In February 2018, then head of FINRA enforcement, Susan Schroeder, remarked that enforcement action “is not the right tool in all cases.” Schroeder highlighted that “FINRA often identifies rule violations and addresses them within the examination process” and that FINRA “want[ed] to avoid any perception of ‘rulemaking by enforcement.’”

Although the number of disciplinary actions against firms and individuals filed by FINRA continued to decline throughout the first Trump administration (854 in 2019 and 808 in 2020), we did not observe the same dramatic drop-off that took place after the implementation of FINRA360. Notably, the slow downward trend in enforcement activity continued during the pro-regulation Biden administration, culminating in only 544 new disciplinary actions (letters of acceptance, waiver and consent plus complaints) being filed in 2024. This further suggests that the reorientation of FINRA’s enforcement agenda was driven by internal reforms, not the occupant of the White House.

New disciplinary actions filed by FINRA

While there has been increased bipartisan criticism of FINRA in recent months, including calls to abolish FINRA and fold its regulatory functions into the SEC, we are unaware of any past or future Trump officials publicly endorsing these positions. In fact, one sitting Republican SEC commissioner has previously communicated little appetite for making significant changes to FINRA. Shortly after the implementation of FINRA360, Commissioner Hester Peirce, a Trump appointee who authored a paper critical of FINRA before joining the SEC, expressed cautious optimism about FINRA’s internal reforms along with a desire “to give FINRA space to make changes itself.”

The Future

While history tells us that reforming FINRA will not be at the top of President Trump’s agenda, that does not necessarily mean the change in administration will leave FINRA untouched.

For example, a more constrained SEC opens the door for more, not less, enforcement activity by FINRA in 2025. If, as anticipated, a Republican-led SEC shifts its focus away from internal control issues (e.g., off-channel communications recordkeeping), enforcement of these matters will likely fall to FINRA. The change in administration will also usher in an SEC that is friendlier to the crypto industry, which could lead to more FINRA enforcement actions related to digital assets. In guidance published in August 2024, FINRA signaled that it is closely monitoring its member firms’ crypto-related activities for potential violations.

FINRA has been positioning itself financially to take on increased regulatory and oversight responsibilities. In November 2024, FINRA filed a proposed rule change that would raise member fees to fund investments in technology and increased headcount. The proposed rule change is projected to generate additional annual revenue of between $40 million and $160 million from 2025 through 2029.

On the other hand, constitutional challenges to FINRA’s authority as a private regulator could invite renewed scrutiny of its enforcement powers. In a decision issued in November 2024, the D.C. Circuit Court of Appeals held that FINRA’s expulsion of a member firm that took effect prior to the SEC having an opportunity to review FINRA’s decision likely violates the private nondelegation doctrine, which requires the government to supervise a private entity that has been delegated a regulatory role. The decision left unanswered many important questions about the constitutionality of FINRA’s regulatory authority. Given the Trump administration’s intent to pare back the administrative and regulatory state, future court rulings placing limits on private regulatory bodies would provide an opportunity for, if not compel, a Republican-led SEC to reconsider the authority it has delegated to FINRA.